by Augusto Ninni[1]

As energy accounts for around 2/3 of GHG (greenhouse gases) emissions, we focalize our analysis about the effects of mitigation policies against climate change on energy, particularly electrical energy: so our key issue is energy transition.

The energy trilemma

Since few years the choice between energy sources and more generally energy policies are influenced in most countries by the energy trilemma[2]. That means the design and the assessment of national energy policy must take into account – possibly in the same time - three main issues: affordability-sustainability-reliability.

Affordability means taking into account the cost of energy sources. Even if energy expenditure does not represent the highest cost item for every industry[3] it affects every of them, so that its total weight is very relevant. So, one of the most important changes in the very recent years is the cost reduction of the renewable energies, at least in the generation of electrical energy, to levels lowest than the fossil fuels to make them competitive with the fossil fuels, removing the “grid parity” issue.

Sustainability means considering GHG emissions. There is no doubt that there are strong differences between renewable sources (where emissions are practically zero) and fossil sources, where coal is known to be the most polluting source. This difference is also confirmed if we take into account emissions related to the entire product life cycle, i.e. considering the stages of production of raw materials and semi-finished products, manufacture of components, and then waste disposal.

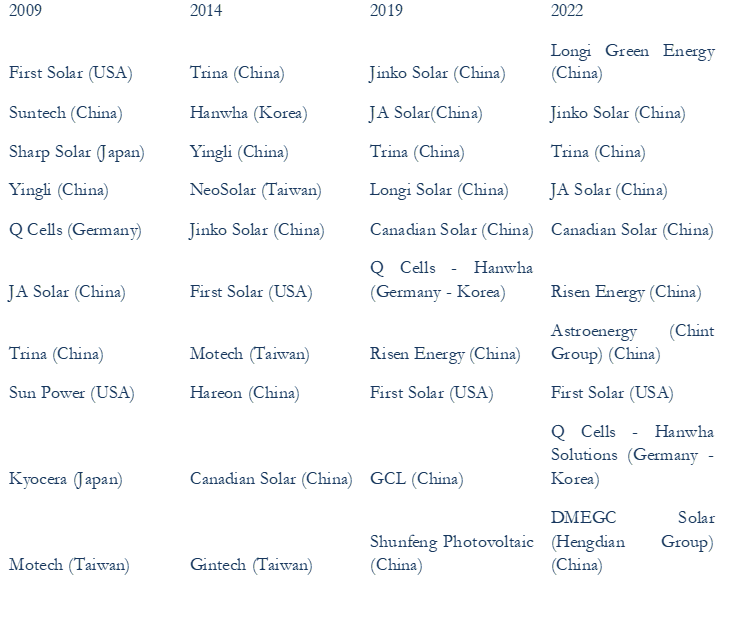

Reliability means reducing dependence on foreign sources, both for the final product and for upstream stages. The incidence of this argument is strongly increasing in very recent times[4] after the Russia-Ukraine war, but it is affecting also the future of the energy transition, give the absolute supremacy of China in the PV (photovoltaic) industry. Its share in the world solar panel exports is more than 70 % while - according to IEA (International Energy Agency) - its production capacity overcomes 90 % of the world total for some components of the PV chain. Less known is the evolution of the Chinese firms in the world industry, moving from 2009 (when the domestic demand accounted around for 5% of its capacity) to 2022 (where eight top companies on ten are Chinese (table 1).

TAB. 1 - The top 10 photovoltaic companies in the world, in terms of quantity sold.

Sources: for 2009 and 2014 Renewable Energy World; for 2019 SolarQuotes; for 2022 Pv-Tech

Industrial policies of US and EU

So, US and EU are developing their own industrial policies[5] to support inside energy transition also by trying of reducing their dependence on China.

A few months after the invasion of Ukraine, in August 2022 Biden's United States launched the Inflation Reduction Act (IRA), a vast intervention programme: one of the aims of which was to facilitate the development of renewable energies while adding the strategic objective of reducing economic dependence on foreign countries, not changing too much the approach followed at the time by Donald Trump.

IRA is one of the best examples of how it is possible to reduce (and strongly) the emissions of the production system while at the same time favouring employment and productive development, so as to dispel that negative image of lowering social welfare with which energy transition is sometimes presented. In the IRA, out of an intervention programme worth 499 billion dollars (over ten years, with an equal share year by year), 'climate and energy' counts for 391 billion, of which 41% for renewable energies and 9% for electric vehicles, in the form of tax credits and subsidies, providing some “protectionist” measures, based on local content requirements (LCR).

For example:

- «clean energy sources»: tax credits are increased by 10% if made in North America steel and other components are used

- Electric vehicles: customers can receive credits only if vehicles utilize some percentages of materials and components, or parts of batteries coming from US (or countries with foreign change agreements).

The main critics are that LCR attracts foreign investments (and discourage US firms to go abroad); furthermore, LCR is against WTO (World Trade Organization) rules[6].

Less than one year after the IRA, the European Commission proposed a plan to facilitate the development of renewables: here too, paying particular attention to reducing dependence on foreign countries (and China in particular), albeit in a different form from the IRA approach, but also responding to the increased attractiveness of locating these plants in the USA, due to the “appeal” of the IRA protectionist measures.

The name of the EU proposal[7] is the Net Zero Industry Act (NZIA). The NZIA proposal is less generous[8] than the IRA in terms of funds, and probably less realistic in terms of objectives (it aims to reach self-sufficiency of 40 % by 2030 in clean technologies).

In terms of reliability, it introduces the concept of strategic dependence (if supply concentration from a foreign country is around 65, to lower to 50% in some cases) to be utilized in auctions and Government Public Procurement of components for clean energy.

So the main difference is clear: for the reduction of the dependence from abroad IRA utilizes a sort of Buy American approach (albeit for some components plus EV and batteries), while NZIA does not utilize a Buy European approach, as it prefers to look at the concentration of supply.

Effects on emerging countries

Energy transition (from fossil fuels to renewables energy sources, RES) affects the industrial features of the emerging countries mainly in two, interconnected but different, ways:

- The inside manufacturing for RES, which derives from the industrial policy of the country also in order to achieve its NDCs (Nationally Determined Contibution);

- The amount of exports of components for RES, which is influenced by possible use of local content and other clauses of commercial policy, deriving from the industrial policies of other countries.

The first way is rather simple to assess. We looked at the plans of industrial policies of some Asian and African emerging countries (as they are summarized in English), searching where the term “manufacturing for renewables” is officially mentioned between strategic industries for the current or for the future times, and where the term “photovoltaic” industry is explicitly utilized among them (see Table 2).

The result is straightforward: all the considered countries mention both “manufacturing for renewables” and “photovoltaic” as a part of the development plans, Egypt being the only exception.

TABLE 2 – “MANUFACTURING FOR RENEWABLES” AND “PHOTOVOLTAIC” TERMS IN THE INDUSTRIAL PLANS OF EMERGING COUNTRIES

|

Manufacturing for Renewables as a strategic industry |

Photovoltaic |

Explicit import limitations (local content and other) |

|

|

China |

v |

v |

|

|

Egypt |

Wind and CSP (concentrated solar power) |

Wind and CSP |

|

|

India |

v |

v |

V |

|

Indonesia |

v |

v |

V |

|

Malaysia |

v |

v |

V |

|

Morocco |

v |

v |

V |

|

Saudi Arabia |

v |

v |

V |

|

South Africa |

v |

v |

V |

|

Thailand |

v |

v |

|

|

Turkey |

v |

v |

V |

|

Vietnam |

v |

v |

Leaving aside China, the issue is worthwhile for India, where according to Ieefa (Institute for Energy Economics and Financial Analysis) India’s industrial policy efforts have focused on solar PV.

The Indian Government has taken several actions to address this situation. Besides tariffs (a basic customs duty, BCD), non-tariff import restrictions (the Approved List of Models and Manufacturers, ALMM) and domestic content requirements, it implemented a production linked incentive (PLI) scheme for solar PV manufacturing in April 2021.

Note that as in EU cell, ingot/wafer and polysilicon production capacity, however, remains marginal or non-existent, with module and cell production being the focus of PLI funding. That means that Chinese supremacy in the production of low value added components are expected not to be defeated[9].

Thus, it seems that up to now, it seems that up to now the effects on emerging countries of US and EU industrial policies are rather small for China, which counts also on a very important expected domestic energy demand[10]; more interesting (after 2026-2027) for India, maybe interesting for ASEAN countries, benefitting from Chinese FDI (foreing direct investments) , and for countries of North Africa (mainly Egypt and Maroc), benefitting from EU FDI.

Bibliography

Claeys, Gregory, 2023 - 'The Net Zero Industry Act puts EU credibility at risk', Bruegel's First Glance, 17 March 2023

Cozzi. Laura - Green Transition and Energy Industry: The Key Role of Technological Innovation in ISPI, The Comeback of Industrial Policy, 2023

IEA, 2022 – International Energy Agency, “Special Report on Solar PV Global Supply Chains”, Parigi 2022;

IEA 2023a - International Energy Agency, Energy Technology Perspectives, Parigi, 2023

IEA 2023 b – Renewable Energy Market Update, Parigi 2023

IIEFA, 2023 – IIEFA-JMK, “New paradigms of Global Solar Supply Chain”, 2023

Ninni, Augusto - «Transizione energetica e politiche industriali: Stati Uniti ed Europa a confronto», L’Industria 2023, forthcoming

Scheifele-Braüning-Probst, «The impact of local content requirements on the development of export competitiveness in solar and wind technologies”, Renewable and Sustainable Energy Reviews, 20220

[1] OEET and Mercatorum University, Rome,

[2] It is an approach institutionalized at the time by the World Energy Council, a long-standing international association of energy experts.

[3] Of course with the exception of the energy intensive industries.

[4] The strategic factor was very important also in the past: the increasing weight of the European investments in the nuclear energy started with the first crisis of the Suez channel (1956).

[5] Industrial policies connected with energy policies, aiming at managing the last in order to improve at least competitiveness, are not unknown: remember at least the examples of France (nuclear energyr) and Germany (Energiewende).

[6] However we must take into account the refusal of the Biden Administration to nominate US delegates in the Appellate Body of WTO, so WTO meets some difficulties to work out.

[7] In October 2023 approved also by the European Parliament: the European Council has not yet discussed it.

[8] According to Gregory Claeys' first comment, 2023: the additional lack - in terms of available funds - of the NZIA is due to the 'political' characteristic of the act, i.e. it is proposed to please some countries, while the lack in terms of disbursements serves to please other countries.

[9] It is possible that China shifts the PV low value added components in ASEAN countries components, as it made during the commercial war during the Trunmp Administration.

[10] Scale economies are very important in the PV industry: so a large domestic demand decreases unit costs.