By Nora Aboushady[*] and Chahir Zaki[§]

An increasing part of today’s international trade takes the form of Global Value Chains (GVCs). According to the estimations of the OECD, about 70% of international trade involves GVCs, as raw materials, intermediate goods, and services cross the borders several times to be incorporated into the final product.[1] GVC activities are also affected by the firm’s decision to outsource parts of the production process or invest in other countries where there is a comparative advantage related to costs or factor endowments. GVCs represent therefore a promising opportunity for developing countries to find a place in the international market by producing and exporting along these chains, to attract foreign investments if their markets are competitive, and to harmonize production standards and acquire international certifications. This will help them increase and diversify their exports and export destinations.

The determinants of one country’s participation in GVCs is therefore not only related to its production and export structure, but also to its overall investment climate and trade policy in place (Dovis and Zaki, 2020). The quality of institutions and the prevalence of informal practices and corruption also affect the overall transparency and competitiveness of markets and firms’ potential engagement in GVCs.

The Egyptian case is of particular interest. In fact, the country’s integration in GVCs remains relatively limited. Despite serious investment and trade policy reforms, Egypt -as the rest of the MENA region- continues to perform weakly in international trade. Compared to other regions, the MENA region has a modest share of firms that are large and/or productive enough to engage in GVCs. In this article, we explore the reasons behind Egypt’s weak GVC integration by focusing on trade policy and political connections and propose policy recommendations to overcome these obstacles.

Egypt’s poor integration in Global Value Chains

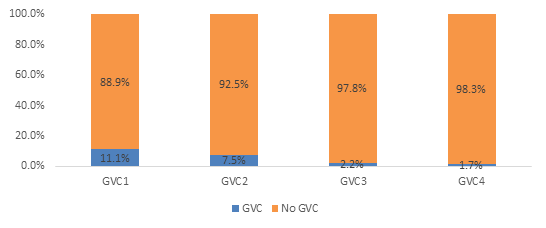

In order to examine the extent of GVC, we rely on the definitions proposed by Dovis and Zaki (2020). The least restrictive form of GVC participation is firms’ exports and imports activity (GVC1). The second indicator of GVC participation adds international certification (often necessary in vertically fragmented production processes) to exports and imports by a firm (GVC2). The third indicator adds foreign ownership to exports and imports, as foreign-owned firms often serve as export platforms (GVC3). The fourth indicator (GVC4) takes into account all four activities (exports, imports, international certification, and foreign ownership) and illustrates deepest form of GVC integration.

Egypt’s GVC participation remains low across the four definitions. Using the simplest definition of GVC participation (exports and imports), only 11.1% of Egyptian firms are found to be engaged in GVC. This ratio is lower than the average of MENA countries (13%). When the indicator is augmented by international certification, only 7.5% of firms are effectively engaged in GVC. The share drops to 2.2% for the third definition, meaning that such modest share of firms are exporters and importers, and have a share of foreign capital. Finally, only 1.7% of Egyptian firms are exporters, importers, have international certification and a share of foreign capital simultaneously. While Egypt’s GVC participation does not deviate significantly from the MENA region’s average, the country as well as the region’s performance is generally lower than other regions like Sub-Saharan Africa.

Figure 1. Share of Egyptian firms engaged in GVC

Source: Authors’ own elaboration using the WBES.

What is at Stake?

Political connections

There is growing evidence on the nexus between politically connected firms, their influence on trade policy and their performance in the global market. In the MENA region, research suggests that tariff liberalization and increasing competition pushed politically connected firms to lobby for increased “hidden protectionism” in the form of non-tariff measures (NTMs) and other behind-the-border policies. For example, positive links were found between politically connected firms and the number of NTMs in sectors with low tariffs in Tunisia.[2] Politically connected firms were also found to be more likely to operate in sectors with higher FDI restrictions.[3] In the case of Egypt, political connections or “crony capitalism” could partially explain the rise in standards in the market: in sectors populated by politically connected firms, a higher share of products subject to NTMs and a higher number of NTMs were observed.[4]

The influence politically connected firms could have on the country’s trade and investment policy is likely to undermine the economy’s competitiveness and its potential to integrate in GVCs. With more severe restrictions on trade and foreign investment, politically connected firms are protected from foreign competition, and other non-connected firms suffer additional barriers to integrate into the global market. Connected firms are also more likely to overcome barriers to entry, operation, and international trade and are more likely to enjoy an easier access to government resources and information, receive special treatment in matters related to investment or trade across borders (for example, inspections and administrative procedures may be overcome more easily by firms with connections).[5] Some studies suggest that politically connected firms are mostly large in size[6], and that State-owned enterprises are more likely to enter the exports market than private sector firms, due to privileged connections and access to information.[7]

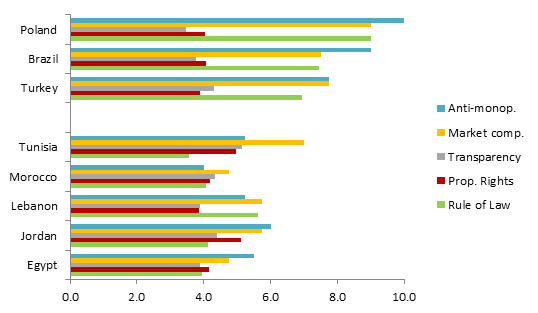

Obviously, such political connectedness is associated to deficient institutions. When Egypt is compared to other economies in the region (Tunisia or Morocco) or outside (Brazil, Turkey or Poland), one can see that it is doing worse in terms of rule of law; anti-monopoly policy and market-based competition (see Figure 2). This confirms how political connections undermine the contestability of the market at both the internal and the external levels.

Figure 2. Institutional barriers

Source: Rule of Law, Market-based competition and Anti-monopoly policy indices come from Bertelsmann Transformation Index. A greater value of the index shows a better performance of the country (from 1 to 10). Property rights and Transparency of government policymaking come from the Global Competitiveness Index. A greater value of the index shows a better performance of the country (from 1 to 10).

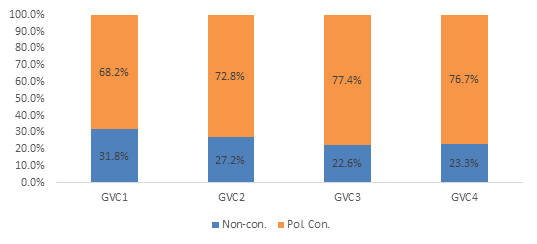

To estimate political connectedness of firms in Egypt, we rely on data from the World Bank Enterprise Surveys for Egypt (2020). A politically connected firm is one where the owner/ CEO/top manager/board member was appointed to a political position. Figure 3 illustrates the share of politically connected firms that engage in GVCs across the four definitions. Among all firms exporting and importing, 68.2% are politically connected. This share increases for the more complex definitions of GVC integration, where 72.8% of firms that export, import, and have international certifications are politically connected. This share increases to 77.4% for firms that have a share of foreign capital, and 76.7% for firms who have the four characteristics of GVC participation.

Figure 3. Political connections and GVC participation

Source: Authors’ own elaboration using the WBES.

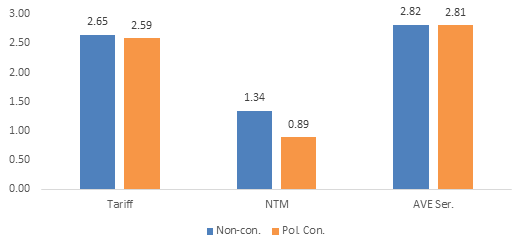

Figure 4 depicts political connectedness and the incidence of trade policy on firms in Egypt. While is it difficult to conclude differentials in the impact of tariffs and services restrictions between politically connected and non-connected firms, the difference is observable for non-tariff measures. In fact, many NTMs could be applied in unequal and non-transparent ways according to the political connectedness the firm enjoys (for example, inspections, licensing, and administrative procedures).

Figure 4. Political connections and trade policy

Source: Authors’ own elaboration using the WBES.

We also run a set of regressions to estimate the impact of the investment climate, the different trade policy measures, and political connections on firms’ GVC participation in Egypt.[8] Our results suggest that political connectedness matters for firms’ integration in GVCs. In fact, the appointment of an owner/ CEO/top manager/board member of the firm to a political position is found to have a positive and significant effect on the firm’s GVC participation across the four definitions discussed earlier in this article. The results from the regressions also suggest that political connections reduce the negative impact of inefficient and restrictive investment- and business regulations. Additionally, trade policy measures in the form of tariff and non-tariff measures reduce the likelihood of firms engaging in GVCs across its four definitions. The next section will analyze more thoroughly these dimensions, namely: investment climate and trade policy.

Further Explanations

At the level of investment climate, Egypt was listed as a top reformer in the MENA region during the period 2004-2008.[9] Along with trade liberalization, market deregulation and privatization, a series of investment-related reforms were carried out to attract foreign investments. The period 2014-2018 is marked by reforms in the investment-related regulations, including tax incentives and additional investment guarantees. Despite these reforms, foreign direct investment represents today less than 3% of GDP[10], a significantly low share as compared to FDI levels following the first reform period and the overall FDI share to GDP before the 2011 uprising. Moreover, only 5% of the country’s total FDI is in the manufacturing sector, while the largest share is concentrated in the oil sector[11]. The concentration of FDI in the oil sector has adverse implications on the potential integration of Egyptian firms in GVCs and their eventual upgrade along the chain towards more value-added sectors.

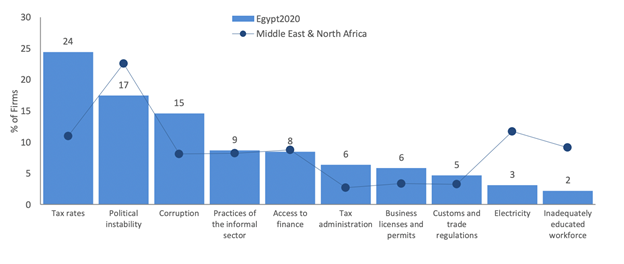

As illustrated in Figure 5, the top three obstacles facing firms operating in Egypt are tax rates, political instability, and corruption. The severity of these obstacles differs by firm size. For example, small and medium firms perceive tax rates as the most severe constraint, while for large firms, the top constraint is corruption. Large firms also suffer from constraints related to access to finance. In fact, access to credit remains one of the major problems affecting investment in Egypt. The share of credit to the private sector in total credit dropped from 54% in 2010 to 30% in 2020.[12] In addition to relatively weak financial intermediation, the generous returns on government-issued bonds crowds-out private investors of the credit market.

Figure 5. Top 10 business environment constraints in Egypt

Source: WBES.

As per trade policy, while tariffs are low in industrialized countries and have largely deceased in developing countries, NTMs and behind-the-border restrictive services regulations impede firms’ participation in the international market. In Egypt, the average tariff rate decreased from 40% in 2002 to 14.4% in 2019. Between 2002 and 2019, the average tariff rate on manufactured products also dropped from 44% to 5%,[13] reflecting the country’s open trade policy and the conclusion of several regional trade agreements. Despite significant liberalization of the domestic market, tariff rates in Egypt remain higher than those in other MENA countries such as Jordan (4.8%).[14] Sectors with a comparative advantage also remain highly protected. For example, the applied tariff rates on food and beverages, apparel, and leather goods, range from 20% to 28%.[15] High tariffs limit the firms’ incentive to increase their productivity and become internationally competitive.

A high number of NTMs also protects some of the potentially competitive sectors. For example, the food and beverages sector alone has over 30 NTMs. Since the gradual reduction in tariff rates, the number of NTMs has increased, suggesting hidden protectionism of domestic production in specific sectors where firms may be politically connected. In fact, Egypt has one of the highest frequency indices and coverage ratios of NTMs among developing countries and has been introducing NTMs faster than its peers.[16] While the use of NTMs could be justified by legitimate purposes related to consumer safety and production standards, NTMs are more often used as an alternative trade policy tool to protect the domestic market from foreign competition. Aside from the market distortions created by the heavy reliance on NTMs, these also affect firms engaged in international trade and GVCs. In fact, Egyptian firms rely heavily on the imported intermediate inputs and equipment. Thus, the impact of NTMs on the cost and availability of imports undermines Egyptian firms’ competitiveness in the international market. Firms in Egypt also suffer from ad-hoc export-related measures that often increase their costs of exports and weakens their position in the international market.

Another potential distortion to international trade is the degree of restrictiveness in the provision and trade of services. Egypt, as well as the MENA region, is among the countries with the highest restrictions on services like professional services, transport, and telecommunications. Despite the country’s commitment to liberalize trade in services in line with it’s the General Agreement on Trade in Services commitments, these liberalization efforts are often offset by burdensome and unnecessary behind-the-border policies. Liberalization of services that support production and exports is likely to generate positive outcomes for the country’s overall competitiveness and can increase Egyptian firms’ participation in GVCs given the servicification of the manufacturing sector.

The Way Forward

The article shows that political connectedness matters for GVC integration. Moreover, our empirical works indicates that the negative impact of investment-related obstacles is reduced for politically connected firms. Thus, in the context where Egypt is to attract investments and increase its share in global trade through better GVC participation, several reforms have to be taken into consideration.

First, increasing transparency and levelling the playing field for firms investing in Egypt is a precondition for better integration in the international market. Thus, there is a need to develop a more transparent state ownership policy and governance framework. Finally, it is important to implement effectively the principle of competitive neutrality to ensure that all actors operate under the same conditions as those governing private sector enterprises.

Second, in terms of trade policy, hidden protectionism from trade policy measures and political connections are likely to offset liberalization efforts and potential investment-related reforms. This is why making non-tariff measures more transparent and more evidence-based will make them more predictable and thus reduce the negative impact on GVC integration.

Finally, in order to attract FDI in the manufacturing and encourage Egyptian firms to integrate into GVC, deeper and more structural reforms are needed to improve the business environment, especially in terms of easiness of business permits, access to finance and tax policy.

References

Abdel-Latif, H., & Aly, H. Y. (2018). “Are politically connected firms turtles or gazelles? Evidence from the Egyptian uprising. Evidence from the Egyptian Uprising”, Economic Research Forum, Working Paper N.1304.

Aboushady, N., Kamal, Y. and Zaki, C. (2021). “Disentangling the Impact of Trade Barriers on Wages: Evidence from the MENA Region”, Middle East Development Journal (forthcoming).

Aboushady, N. and Zaki, C. (2021). “Hidden Protectionism and Global Value Chains Integration: Evidence from Egyptian Firms”, (forthcoming).

Aboushady, N. and Zaki, C. (2019). “Investment Climate and Trade Margins in Egypt: Which Factors Do Matter?”, Economics Bulletin, vol.39, issue 4, pages 2275-2301.

Dovis, M. and Zaki, C. (2020) “Global Value Chains and Local Business Environments: Which Factors Do Really Matter in Developing Countries?”, Review of Industrial Organization, vol. 57, pages 481-513.

Eibl, M. F., & Malik, A. (2016). The Politics of Partial Liberalization: Cronyism and Non-Tariff Protection in Mubarak's Egypt.

Eissa, A. M., & Eliwa, Y. (2021). The effect of political connections on firm performance: evidence from Egypt. Asian Review of Accounting, vol. 29(3).

Kruse, H. W., Martínez-Zarzoso, I., & Baghdadi, L. (2021). Standards and political connections: Evidence from Tunisia. Journal of Development Economics, 153, 102731.

World Bank & IFC. (2020). “Creating Markets in Egypt: realizing the full potential of a productive private sector”. Country Private Sector Diagnostics.

[*] Assistant Professor, Faculty of Economics and Political Science, Cairo University, Egypt; E-mail:

[§] Associate Professor, Faculty of Economics and Political Science, Cairo University, Egypt; E-mail:

[1] https://www.oecd.org/trade/topics/global-value-chains-and-trade/

[2] Kruse et al. (2021).

[3] Rijkers et al. (2017).

[4] Eibl and Malik (2016).

[5] Eissa and Eliwa (2021).

[6] Abdel Latif and Aly (2019)

[7] Aboushady and Zaki (2019).

[8] Aboushady and Zaki (forthcoming).

[9] Doing Business Data.

[10] World Development Indicators.

[11] Central Bank of Egypt’s Economic Review Reports.

[12] World Bank and IFC (2020)

[13] World Development Indicators

[14] Aboushady et al. (2021).

[15] WITS

[16] World Bank and IFC (2020)