by Andrea Boltho[*]

The text that follows briefly looks at changes in the revealed comparative advantage indices of four East Asian countries (Japan, South Korea, Taiwan and China) over half a century or more for the capital intensive and increasingly high-tech sector of machinery and transport equipment. This covers industries which were considered as totally unsuited to what were relatively poor and labour-abundant economies, whose comparative advantage was seen to lie in simple labour-intensive consumer goods and semi-manufactures. Yet, despite this conventional wisdom, governments in all the four countries actively encouraged in a variety of ways the growth of advanced manufacturing companies. The undoubted successes that were achieved suggest that such unorthodox policies must have played an important role.

Introduction

The basic elements of East Asia’s success story are well known. At the outset of their respective take-offs (Japan in, say, 1950, South Korea, henceforth Korea, and Taiwan in about 1960, China around 1980), the four countries were relatively poor. Japan’s per capita GDP in purchasing power parities stood in 1950 at barely 20 per cent of the US level. Korea and Taiwan in 1960 were barely at the level of Sub-Saharan Africa, while China was below that level in 1980. By 2021, Japan, Korea and Taiwan had reached 65 to 90 per cent of the US level, while China, after four decades of above 8 per cent annual growth, was at a 30 per cent level. Hardly any other country, bar the city states of Hong Kong and Singapore, can boast of similar achievements.

Equally well-known are many of the explanations that have been put forward for this exceptional experience. A major investigation by the World Bank stressed a number of features of the East Asian model which were conducive to growth: high rates of savings and investment in both physical and human capital, conservative macroeconomic policies, homogenous societies, competent bureaucracies, etc. (World Bank, 1993). That same investigation, however, attributed only a rather minor role at best to interventionist economic policies, as did a number of other works on this issue (e.g., Little, 1979; Calder, 1993; Little et al., 1994; Beason and Weinstein, 1996; Pack and Saggi, 2006).

This very brief paper takes a new look at the issue by examining not so much the overall growth record but the changes in the comparative advantage of the four countries over the 1950-2020 period. At the outset, these countries were seen as relatively labour abundant developing economies, fit no doubt for simple labour-intensive sectors such as textiles and clothing, but highly unlikely to prosper in advanced manufacturing industries. Today, Japan, Korea and Taiwan are considered high-tech powerhouses while China is close to becoming one. Section I looks at what happened to their comparative advantage in one particular advanced sector. Section II looks for explanations and a final paragraph concludes.

East Asia’s Revealed Comparative Advantage

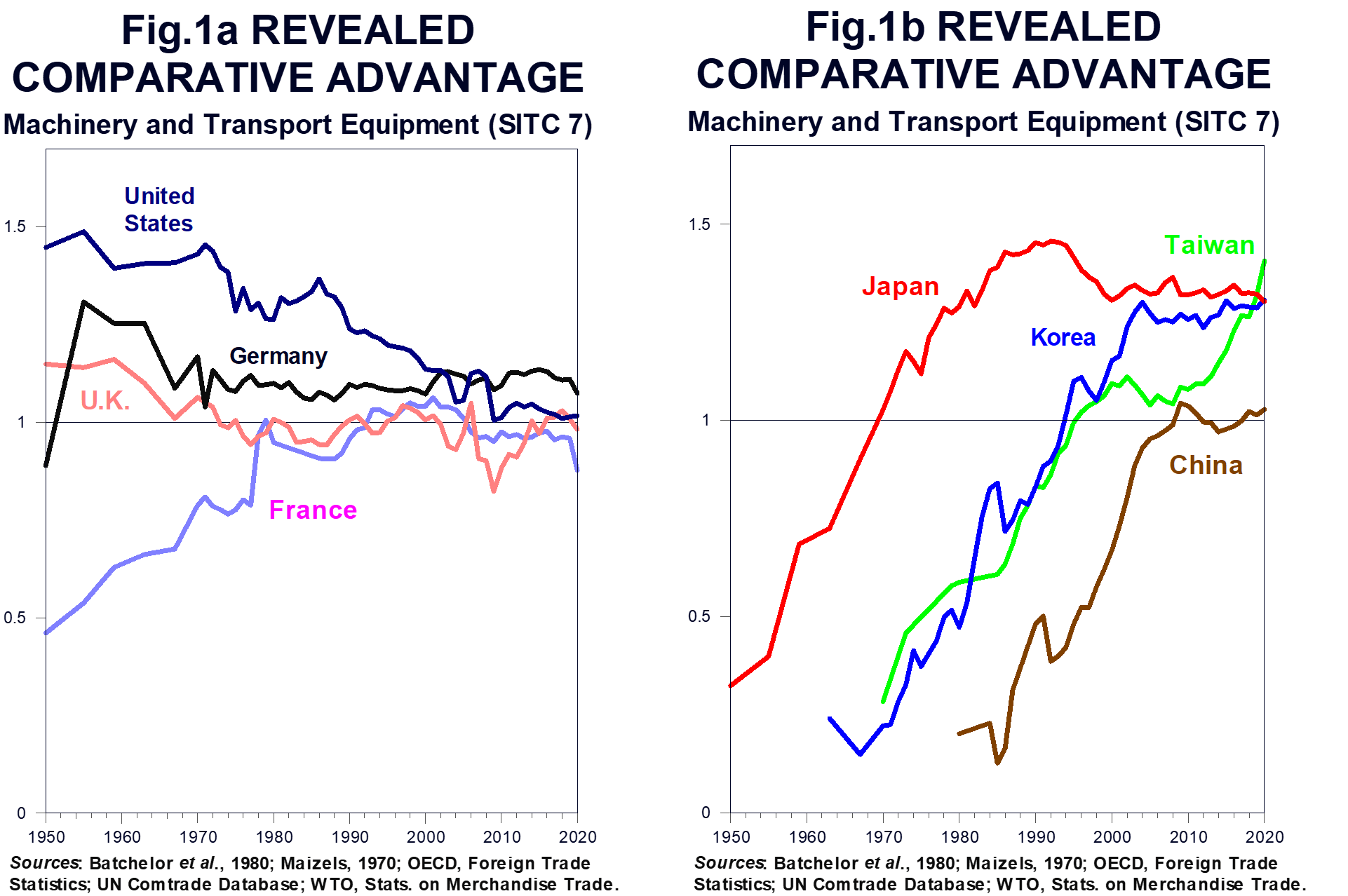

To illustrate the four countries’ changes in comparative advantage over time use is made of the “Revealed comparative advantage” index first used by Balassa (1965). This measures the ratio between a country’s share of world exports in a particular product and its share of total world exports. Any index value above unity suggests that the country in question enjoys an apparent advantage in the world market for that particular product since its presence in that market is above what would normally have been expected given its presence in the world economy. To keep matters simple, the investigation will limit itself to one product category: machinery and transport equipment (or SITC 7 in the standard international trade classification). Though this excludes some advanced chemical and pharmaceutical products, it still encompasses the bulk of high-tech production. Primary products are excluded throughout so that the two denominators in the ratio (a country’s total exports as well as world total exports) only refer to manufactures.

Results are shown in Figure 1 which plots the revealed comparative advantage indices for SITC 7 from 1950 onwards for four large Western countries and for the four East Asian economies here considered. Panel A shows how the United States, Germany and the United Kingdom gradually lost ground from their dominating positions in the 1950s and 1960s. Germany today still has indices above unity, but this is barely the case for the US, the UK let alone France. Panel B turns to East Asia. The results look striking: almost vertical and almost parallel soaring lines at three different points in time. In relatively short time spans, three out of the four countries moved from indices not much above zero at the outset to levels, four or more decades later, significantly above unity. And China has in recent years also moved above that threshold.

Why Did it Happen?

The orthodox view of these successes is that they were primarily the happy result of market forces. Entrepreneurs, little hindered by intrusive government intervention or excessive regulation, spotted opportunities both at home and abroad in relatively capital-intensive or advanced technology activities, invested on a large scale and reaped the ensuing benefits. The rapid growth of the world economy together with its opening to international trade was, of course, a further important facilitating factor as were relative permissive macro-economic policies both at home and abroad. In this view, the interventionist policies of, for instance, Japan’s Ministry of International Trade and Industry (MITI) or of Korea’s Economic Planning Board (EPB) were of limited importance (and not always necessarily welfare enhancing). In China’s case central planning clearly played an important role, but even here export growth resulted mainly from a very dynamic private sector as it also did in Taiwan.

This view leaves something to be desired. To take Japan first, in the early 1950s this was a poor country still ravaged by the aftermath of a very destructive war, importing virtually all its sophisticated manufactured products and relying on labour-intensive clothing and semi-manufactures such as textiles or pottery for its exports. Most observers at the time thought that such a specialization pattern would continue for the foreseeable future. The Bank of Japan, for instance, favoured the development of light industry (Genther, 1990).[1] Others, however, thought that comparative advantage could be created strategically (Gao, 1997) and the country moved rapidly up the value-added scale in the 1950s in sectors which MITI had selected for development, e.g., motorcycles, machine tools, cars or plastic products such as polyethylene. This selection, of course, had nothing to do with “picking winners” which, it is usually (and plausibly) argued, can only be done by risk-taking entrepreneurs, not by bureaucrats. Japan was at the time a follower country and could see from what had happened in more advanced economies what the promising industries were.

An important feature which facilitated this process, more than MITI’s direct intervention, was widespread protectionism.[2] Suffering from a significant balance of payments constraint in a fixed exchange rate world, Japan severely restricted manufactured imports by quotas and tariffs, of course, but more importantly through the allocation of foreign exchange (Takeda, 2000). It is this which allowed Japanese producers to spot opportunities and to massively invest, sure in the knowledge that they would not be priced out by more competitive foreign firms.[3] The investments, in turn, led to the achievement of scale economies and, eventually, to successful exports.

While such infant industry protection has often failed in many developing countries (e.g., Bell et al., 1984), it was successful in Japan for a further and very crucial policy reason. Competition at home was fierce as the major keiretsu conglomerates vied for market share. MITI positively encouraged this competition by, for instance, licensing foreign technology (over the imports of which it had a virtual monopoly) not to one favourite company, but to all or most major firms in each industry. This was true, for instance, for polyethylene (Peck, 1976), synthetic fibres (Ozawa, 1980), steel (Vestal, 1993), or television production (Lynn, 1994). Policy, in other words, fostered competition at home while, at the same time, ensuring protection from abroad. In the words of Krugman (1994) import-substitution generated successful export promotion.

Turning to Korea, the story is not dissimilar. This was also a poor, war-ravaged, country that outsiders saw as destined to export labour-intensive semi-manufactures and cheap consumer goods. The idea that the country could specialize in, say, steel or ship production seemed outrageous in the 1960s. The World Bank, for instance, was scathing in 1960, a time when Koreans were poorer than their contemporaries in, say, Cameroon, Madagascar or Nigeria, about the prospects of a steel industry (Redding, 1999). Yet, this notwithstanding, the Korean government created a new steel company, Posco, in 1973. By 1985, Posco had become one of the world’s lowest cost producers (ibid.). Similarly, the government played an important direct and indirect role in the extremely rapid growth of the country’s very successful shipbuilding industry (Lee, 1990), an initially infant industry which achieved maturity within only a few years after its inception (Bell et al., 1984).

In Korea too competition was seen as crucial for success. Encouraging it at home, as Japan had done, was, however, not really viable. Japan’s large internal market could provide sufficient demand for several competing domestic firms. Korea was too small to offer similar opportunities. What the country did from the mid-1960s onwards was to push Korean companies to compete on the world market, helping them not by protectionism but by various forms of subsidies. These were granted to the larger chaebol conglomerates on condition, however, that they fulfil stringent export targets (Amsden, 1989). Here too, government intervention seems to have played an important role in creating successful exporters, often in machinery, transport equipment and, more recently, in advanced tech sectors.

Taiwan’s economy has, from the outset, shown a higher degree of domestic competition than either Japan or Korea because of the presence of a very large number of small- and medium-sized firms. Government intervention was, however, pervasive here too. Significant support to the manufacturing sector came directly through large public investments, and indirectly via preferential treatment in public purchases, generous tax concessions and depreciation allowances as well as through interest rate subsidies (Rodrik, 1995). In one particular area government support was amazingly successful: semi-conductors. This sector was chosen in 1974 as a key industry and has since received significant R&D funding. One offshoot of this policy is Taiwan’s Semi-conductor Manufacturing Company (TSMC) which benefited from a direct injection of capital from the government at the time of its creation in 1987 (National Research Council, 2003). TMSC had, by 2021, become (together with Samsung) the world’s largest producer of advanced chips,

China was, of course, more interventionist than any of the three other countries. Deng Xiaoping’s reforms did away with the rigid central planning of the Mao Zedong era, but the state retained vast powers of intervention. These were used in helping state enterprises in heavy industry and, increasingly, in high-tech sectors. Subsidized credit was one important instrument, protection against imports another. The success of these policies has become increasingly evident in recent years. China is now explicitly aiming to become a major technological power in areas such as robotics, new energy vehicles, aero-space and, especially, artificial intelligence.

It may be interesting to note that while China promotes national champions in some areas, it also encourages competition. This has been fierce in the very dynamic private sector; it is also present at the regional level with local authorities experimenting with different forms of intervention and deregulation (Bardhan, 2016), and it is not absent in the state sector where companies have been forced to merge or close down. The rapid opening of the economy to foreign trade has also raised the degree of competition. Admittedly however, Xi Jinping’s recent shift towards asserting much greater state control over the economy could be curbing some of these competitive pressures. And this, in turn, would almost certainly reduce the economy’s dynamism.

Conclusions

Summarising, the (admittedly partial and imperfect) evidence suggests that interventionist policies contributed to East Asia’s successes, at least in the relatively advanced and sophisticated sectors here considered. Alternative explanations do not seem to be fully persuasive. No claim is made that this is a firm conclusion. Many other forces were also at work in promoting the export of the four countries, as indicated in the Introduction above. Attributing weights to the various arguments is not attempted and would almost certainly be impossible. But, contrary to received wisdom, industrial policy (widely defined) may, after all and despite many errors, have had welfare enhancing effects. This unorthodox conclusion is, however, tempered by one important consideration: East Asia’s experience was no doubt exceptional in large measure because the area benefited from some exceptional features that are not often present in many other developing countries: high levels of human capital at the outset, relatively competent bureaucracies, less corruption than elsewhere (certainly in Japan and Taiwan, probably in Korea, at least in more recent years and, possibly, also in China), political stability throughout (other than in Korea at times). Protectionism, in other words, could well have led to semi-stagnation, while “picking winners” might have degenerated into rent-seeking had it not been for these crucial socio-economic pre-conditions.

References

Amsden, A. (1989), Asia’ Next Giant: South Korea and Late Industrialization, Oxford University Press, New York, NY.

Balassa, B. (1965), “Trade Liberalisation and Revealed Comparative Advantage”, The Manchester School, Vol.33, No.2, May, 99-123.

Bardhan, P. (2016), “State and Development: The Need for a Reappraisal of the Current Literature”, Journal of Economic Literature, Vol.54, No.3, September, 862-92.

Beason, R. and D.E.W Weinstein (1996), “Growth, Economies of Scale and Targeting in Japan (1955-1990)”, Review of Economics and Statistics, Vol.78, No.2, May, 286-95.

Bell, M., B. Ross-Larson and L.E. Westphal (1984), “Assessing the Performance of Infant Industries”, Journal of Development Economics, Vol.16, No.1-2, September-October, 101-28.

Calder, K.E. (1993), Strategic Capitalism – Private Business and Public Purpose in Japanese Industrial Finance, Princeton University Press, Princeton, NJ.

Clemens, M.A. and J.G. Williamson (2004), “Why Did the Tariff-Growth Correlation Change after 1950?”, Journal of Economic Growth, Vol.9, No.1, March, 5-46.

Gao, B. (1997), Economic Ideology and Japanese Industrial Policy, Cambridge University Press, Cambridge.

Genther, P.A. (1990), A History of Japan’s Government-Business relationship: The Passenger Car Industry, University of Michigan Press, Ann Arbor, MI.

Itoh, M., K.Kiyono, M.Okuno and K.Suzumura (1988), “Industry Promotion and Trade”, in R.Komiya, M.Okuno and K.Suzumura (eds.), Industrial Policy of Japan, Academic Press Inc., Tokyo.

Krugman, P.R. (1994), “Import Protection as Export Promotion: International Competition in the Presence of Oligopoly and Economies of Scale”, in H. Kierzkowski (ed.), Monopolistic Competition and International Trade, Oxford University Press, Oxford.

Lee, T-W. (1990), “Korean Shipping Policy: The Role of Government”, Marine Policy, Vol.14, No.5, September, 421-37.

Little, I.M.D. (1979), “An Economic Renaissance”, in W. Galenson (ed.), Economic Growth and Structural Change in Taiwan, Cornell University Press, Ithaca, NY.

Little, I.M.D., R.G.Lipsey and S.Togan (1994), “Trade and Industrialisation Revisited”, The Pakistan Development Review, Vol.33, No.4, Winter, 359-89.

Lynn, L.H. (1994), “MITI’s Successes and Failures in Controlling Japan’s Technology Imports”, Center for International Studies, Massachusetts Institute of Technology, Working Paper, MITJP 94-11.

National Research Council (2003), Securing the Future: Regional and National Programs to Support the Semiconductor Industry, The National Academies Press, Washington, DC.

O’Brien, P.K., T. Griffiths and W. Hunt (1991), “Political Components of the Industrial Revolution: Parliament and the English Cotton Textile Industry, 1660-1774”, Economic History Review, Vol.44, No.3, August, 395-423.

O’Rourke, K.H. (2000), “Tariffs and Growth in the Late 19th Century”, Economic Journal, Vol.100, No.463, April, 456-83.

Ozawa, T. (1980), “Government Control over Technology Acquisition and Firms’ Entry into New Sectors: The Experience of Japan’s Synthetic-fibre Industry”, Cambridge Journal of Economics, Vol.4, No.2, June, 133-46.

Pack, H. and K. Saggi (2006), “Is There a Case for Industrial Policy? A Critical Survey”, World Bank Research Observer, Vol. 21, No.2, Fall, 267-97.

Peck, M.J. (1976), “Technology”, in H.Patrick and H.Rosovsky (eds.), Asia’s New Giant: How the Japanese Economy Works, Brookings Institution, Washington, DC.

Redding, S. (1999), “Dynamic Comparative Advantage and the Welfare Effects of Trade”, Oxford Economic Papers, Vol.51, No.1, January, 15-39.

Rodrik, D. (1995), “Getting Intervention Right: How South Korea and Taiwan Grew Rich”, Economic Policy, No.20, April, 53-107.

Takeda, H. (2000), “Attainment of Economic Self-Support”, in M.Sumiya (ed.), A History of Japanese Trade and Industrial Policy, Oxford University Press, Oxford.

Vestal, J.E. (1993), Planning for Change: Industrial Policy and Japanese Economic Development, 1945-1990, Clarendon Press, Oxford.

World Bank (1993), The East Asian Miracle, Oxford University Press, New York, NY.

[*] Magdalene College, University of Oxford

[1] An American advisor in the early 1950s apparently thought that Japan should base its economy “… on exports of textile products, raising chickens and exporting eggs, and developing tourism” (quoted in Gao, 1997, pp.209-10).

[2] Following its widespread adoption during the Great Depression, protectionism has, understandably, been widely condemned. At the time its impact was disastrous. But earlier episodes of protectionism suggest that it helped some countries develop successful industries. The best-known example is Britain’s cotton manufacturing which grew very rapidly during the economy’s industrial revolution thanks to initial tariffs on, and a later ban of, India’s textile exports (O’Brien et al., 1991). And research has suggested a causal link between protectionism and growth in a number of countries in the 19th century (O’Rourke, 2000; Clemens and Williamson, 2004).

[3] As was argued in a book that is, otherwise, very sceptical about Japan’s industrial policies: “It cannot be denied that in the 1950s and 1960s the government, with its heavy-handed protection of domestic industry through trade policy, played an important role in assisting the establishment of a number of industries” (Itoh et al., 1988, p.274).